The Diffusion of Financial Literacy Through Interactive Design

by Dhyan Subramani

by Dhyan Subramani

(Image 1 of 6)

Introduction

Financial literacy is widely recognized as a foundational component of economic participation, influencing individuals’ ability to manage debt, budget effectively, save for emergencies, and make informed investment decisions. Despite its importance, global levels of financial literacy remain uneven, with large segments of the population lacking basic financial knowledge (Lusardi & Mitchell, 2014). Traditional approaches to financial education—such as classroom instruction, printed materials, and short-term workshops—have often produced limited long-term behavioral change (Fernandes et al., 2014).

In response to these challenges, the financial technology (FinTech) sector has increasingly integrated educational components into mobile applications. Interactive FinTech applications embed financial learning directly into routine financial activities, allowing users to acquire financial skills through repeated, real-time engagement rather than passive instruction. Central to this shift is gamification, which incorporates elements such as progress tracking, challenges, rewards, and feedback loops to increase motivation and retention (Hamari et al., 2014).

Industry estimates indicate that approximately one-third of personal finance applications now incorporate gamified or interactive learning features (CoinLaw, 2025). As shown in Figure 1, global smartphone and mobile network subscriptions have expanded rapidly, reflecting increased reliance on mobile platforms for everyday financial management and enabling widespread adoption of mobile FinTech applications. These developments suggest that interactive FinTech tools may offer a scalable and behaviorally effective approach to improving financial literacy across diverse populations.

This paper explores the diffusion of financial literacy through interactive FinTech applications by examining design mechanisms, adoption trends, and behavioral outcomes. A focused case study of Southeast Asia highlights how mobile accessibility and localized content accelerate adoption and enable financial education in emerging markets.

Methodology

This study employs a qualitative comparative analysis of interactive FinTech applications, peer-reviewed academic literature, institutional research, and industry reports 2019 and 2025. Secondary data were collected from academic journals in behavioral economics and educational technology, reports from international organizations such as the OECD and World Bank, and market research publications on FinTech adoption.

The analysis focuses on identifying patterns in how financial literacy concepts are embedded into FinTech platforms through gamification, personalization, and behavioral nudges. A regional case study of Southeast Asia was selected due to its rapid growth in mobile FinTech adoption and its large underbanked population. Data were synthesized thematically to evaluate adoption trends, engagement metrics, and reported behavioral outcomes. While the study does not involve primary data collection, triangulation across multiple credible sources was used to enhance reliability.

The Diffusion of Financial Literacy Through Interactive Design

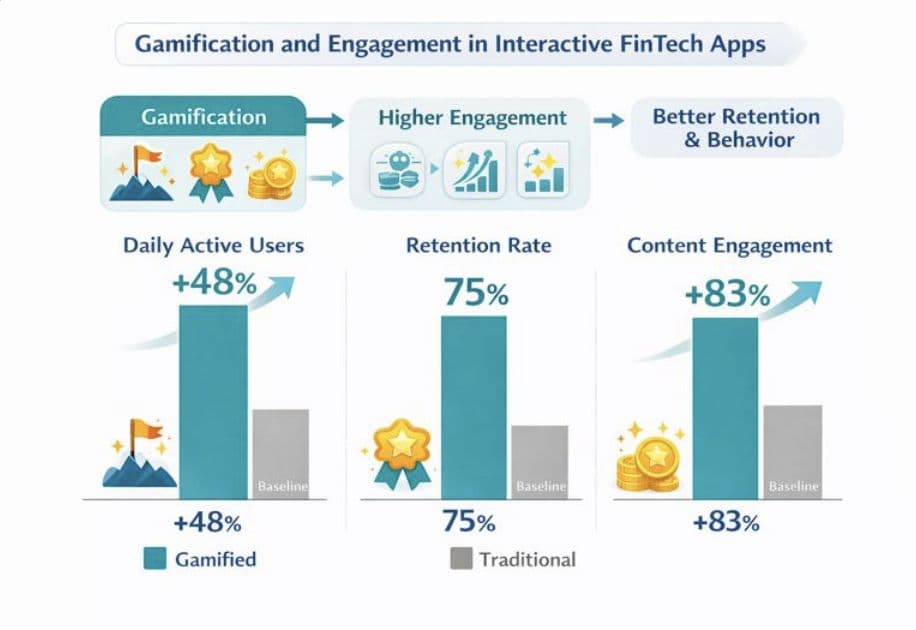

Gamification techniques—such as goal-setting, rewards, progress visualization, and streaks—align financial tasks with intrinsic motivational drivers, including achievement and consistency (Hamari et al., 2014).

Figure 1. Gamification features integrated into interactive FinTech applications, including rewards systems, progress tracking, and behavioral nudges that promote sustained user engagement and financial learning.

Source: Author-created figure adapted from Hamari et al. (2014) and representative FinTech interface features reported in industry literature.

As illustrated in Figure 2, these features are commonly integrated into interactive FinTech applications to promote sustained engagement and reinforce financial learning. These mechanisms transform routine financial activities into experiential learning processes.

Research in educational technology demonstrates that interactive and gamified environments improve engagement and information retention compared to static instructional methods (Dicheva et al., 2015). Within FinTech, sustained engagement enables financial concepts to be reinforced incrementally, increasing the likelihood that users translate knowledge into behavior. Applications such as Revolut and Long Game illustrate how savings and investment goals can be framed as missions or challenges, encouraging consistent financial participation.

Importantly, gamification does not merely increase usage frequency; it reduces cognitive barriers associated with complex financial concepts. By simplifying decision pathways and providing immediate feedback, interactive platforms make financial education more accessible to users with limited prior financial knowledge.

Mobile Accessibility and Global Reach

The diffusion of interactive financial literacy has been strongly shaped by the global expansion of smartphone access. Mobile devices have become the primary channel through which individuals engage with financial services, particularly in regions with limited traditional banking infrastructure. As of 2023, global smartphone subscriptions exceeded 6.6 billion, creating a technological foundation for widespread mobile financial education (Statista, 2024).

Figure 2. Global smartphone and mobile network subscription growth, demonstrating the technological foundation enabling widespread adoption of mobile FinTech applications.

Source: Author-created visualization based on data reported by GSMA (2024) and Statista (2024).

Mobile accessibility enables contextual learning by embedding financial education directly into moments of decision-making, such as budgeting or saving. Many FinTech platforms use AI-driven insights to provide personalized recommendations based on user behavior, reinforcing financial concepts through real-time application. This contextual approach aligns with research showing that learning is more effective when directly tied to practical use (OECD, 2020).

In emerging markets, mobile-first delivery is especially impactful. Platforms that localize content to regional languages, financial norms, and spending patterns demonstrate higher adoption and trust, underscoring the importance of culturally responsive design.

Market Growth and Industry Expansion

The integration of financial literacy features into FinTech applications has coincided with rapid growth in the personal finance app market. Industry analyses estimate that the global personal finance app market surpassed $160 billion in 2025, supported by nearly two billion users worldwide (CoinLaw, 2025).

Figure 3. Growth of the global FinTech market, illustrating increased investment, platform adoption, and industry expansion over time.Source: Author-created visualization based on data from Statista (2024) and Finance Magnates (2023).

As shown in Figure 3, this growth reflects increasing investment, platform adoption, and overall expansion within the global FinTech industry. Gamification has become a key competitive differentiator, with the gamified finance segment projected to grow at a strong compound annual growth rate over the next decade (HTF Market Intelligence, 2025).

Younger demographics, particularly Millennials and Generation Z, represent a substantial share of finance app users and demonstrate strong preferences for platforms that combine automation, education, and interactivity. Technological advancements such as open banking APIs, real-time analytics, and AI-driven personalization continue to expand the scope of interactive financial learning.

Impacts on Financial Literacy and Economic Behavior

Peer-reviewed research indicates that financial education alone does not consistently produce behavioral change; however, interventions embedded in real-world decision contexts show stronger effects (Fernandes et al., 2014). Interactive FinTech applications address this limitation by integrating education into everyday financial behavior.

Studies suggest that sustained engagement with interactive platforms is associated with improved savings behavior, budgeting accuracy, and financial confidence (Lusardi & Mitchell, 2014).

Figure 4. Observed impacts of interactive FinTech application usage on financial literacy outcomes and economic behavior, including budgeting frequency, savings participation, and investment confidence.Source: Author-created conceptual figure synthesized from OECD (2020) and Lusardi and Mitchell (2014).

As shown in Figure 4, users of interactive FinTech applications demonstrate higher budgeting frequency, increased savings participation, and greater investment confidence. Gamified environments increase retention and motivation, allowing users to repeatedly apply financial concepts over time. These effects are particularly pronounced among younger users, who are more likely to manage finances digitally.

At a broader level, improved financial literacy contributes to reduced financial stress, better preparedness for long-term financial commitments, and increased participation in formal financial systems (OECD, 2023).

The behavioral impact of interactive tools is particularly relevant for younger generations. Gen Z and Millennials are among the most active users of mobile financial tools; surveys indicate that over 80% of Gen Z prefer managing finances via mobile apps rather than traditional bank visits, driven by convenience, real-time feedback, and personalization (CoinLaw, 2025).

This intersection of technology and education is especially powerful because it taps into everyday financial decision moments — from tracking a grocery budget to adjusting savings based on unexpected expenses — making the learning experience both immediate and applicable.

Case Study: Gamified Financial Literacy in Southeast Asia

Southeast Asia is one of the fastest‑growing regions for mobile FinTech adoption, providing a compelling real‑world example of how interactive financial literacy can spread and deliver meaningful outcomes.

Figure 5. Adoption of interactive financial literacy features in FinTech applications in the Philippines and Indonesia, highlighting user engagement with budgeting, savings, and investment tools.Source: Author-created visualization based on Finance Magnates (2024) and regional FinTech adoption reports.

Recent research shows that mobile FinTech app penetration in Southeast Asia reached 49% in 2024, up from just 9% in 2019, and †is forecast to reach 60% by 2030. As displayed in Figure 5, this adoption is closely linked to user engagement with budgeting, savings, and investment tools in countries such as the Philippines and Indonesia. The Philippines, in particular, leads the region with a 63% adoption rate, followed by Malaysia (55%) and Indonesia (49%). Finance Magnates

These adoption rates reflect not only increasing smartphone and internet access but also targeted efforts by fintech providers to serve diverse user needs through localized content, culturally relevant interfaces, and integration with widely used platforms. In the Philippines, a high proportion of users — in some studies nearly 80% — report using mobile apps for personal financial tasks, including budgeting, payments, and financial planning. MARKETECH APAC

Partnerships between financial education platforms, local banks, and telecom providers have further expanded reach. These collaborations often embed gamified learning modules into popular mobile wallets and digital banks, making financial education part of everyday financial activity rather than a standalone experience.

Moreover, many markets in the region retain large unbanked or underbanked populations, meaning mobile interactive tools provide one of the few accessible pathways to formal financial learning and engagement. In the Philippines, for example, nearly half of adults remained unbanked even amid rapid mobile adoption, underscoring the continued need for accessible digital financial education (World Bank, 2023).

Across Southeast Asia, fintech adoption trends demonstrate that youthful demographics, expanding mobile connectivity, and supportive regulatory environments combine to create fertile ground for interactive financial literacy tools. These platforms not only teach users about financial concepts but enable them to apply that knowledge directly within apps they already use for payments, savings, and daily money management.

Analysis

The integration of financial literacy into interactive FinTech applications represents a shift from passive education toward experiential, behavior-centered learning. By combining gamification, personalization, and real-time feedback, these platforms promote habit formation and reinforce learning through repeated action.

However, these benefits are not universal. As portrayed in Figure 6, digital divides persist across regions, particularly in rural and low-income areas, limiting access to FinTech platforms for some populations. Digital divides persist in rural and low-income regions, limiting access for some populations. Additionally, poorly designed gamification systems may prioritize short-term engagement over deep understanding, while excessive reliance on behavioral nudges raises ethical concerns regarding manipulation, transparency, and data privacy (Gomber et al., 2018).

The long-term effectiveness of interactive financial literacy initiatives depends on thoughtful alignment between pedagogy, technology, and accessibility. When designed responsibly, these platforms can promote financial inclusion and economic resilience at scale.

Figure 6. Global engagement with FinTech platforms across regions, highlighting varying adoption levels and access disparities between developed and emerging markets.

Source: Author-created visualization based on IMF (2020) and World Bank (2023).

However, these benefits are contingent on addressing critical barriers. Digital divides, particularly in rural regions or low-income areas, limit access for some populations. Even when devices and connectivity exist, uneven digital literacy can prevent effective engagement. Additionally, the design of gamified systems requires careful balance: overly simplistic reward mechanisms may encourage short-term engagement without fostering deeper understanding, while overly complex systems may overwhelm users, reducing long-term retention. Data privacy and ethical handling of user information also remain central concerns; financial literacy apps often collect sensitive behavioral and transaction data, which must be safeguarded against misuse.

Ultimately, the success of interactive financial literacy in driving real-world economic benefits depends on the alignment of technology, pedagogy, and accessibility. When these elements are thoughtfully integrated, mobile platforms can amplify financial knowledge, improve decision-making, and empower users to actively participate in both local and global economies.

Discussion

This study indicates that the diffusion of financial literacy tools through interactive FinTech applications is driven primarily by how educational content is integrated into everyday financial behavior rather than by the quantity of information provided. Interactive design features such as gamification, personalization, and real-time feedback transform financial education into an experiential process, reinforcing learning through repeated engagement. These mechanisms allow users to apply financial concepts incrementally within routine decision-making contexts, supporting the translation of knowledge into sustained financial behavior.

Gamification functions as a pedagogical tool by reducing cognitive barriers associated with complex financial tasks. As demonstrated in Figures 1 and 4, elements such as progress tracking, goal-setting, and rewards simplify decision pathways and provide immediate feedback, encouraging consistent participation in budgeting, saving, and investing activities. This aligns with prior findings in educational technology that experiential and feedback-driven environments enhance retention and behavioral outcomes compared to passive instructional approaches. Importantly, the effectiveness of these features depends on sustained engagement, suggesting that design quality plays a critical role in long-term financial literacy outcomes.

Mobile accessibility further accelerates diffusion by embedding financial learning directly into moments of financial decision-making. As shown in Figure 2, widespread smartphone adoption enables contextual learning through personalized prompts and real-time insights, which reinforce financial concepts when users are most likely to act on them. The Southeast Asia case study illustrates how mobile-first delivery, combined with localized content and culturally responsive design, enhances adoption and trust in underbanked markets, as reflected in the engagement patterns shown in Figure 5.

Despite these advantages, the diffusion of interactive financial literacy is constrained by persistent digital divides and ethical design considerations. As illustrated in Figure 6, uneven access to devices, connectivity, and digital skills limits participation for some populations. Additionally, poorly designed gamification systems may prioritize short-term engagement over meaningful learning, while extensive use of behavioral nudges raises concerns related to transparency, autonomy, and data privacy. These findings suggest that the long-term effectiveness of interactive financial literacy initiatives depends on responsible design choices that balance engagement, accessibility, and ethical accountability.

Limitations

This study relies on secondary data from academic, institutional, and industry sources, which may vary in methodology and reporting standards. Reported engagement and behavioral outcomes may be subject to selection bias, as users who adopt interactive FinTech applications may already possess higher baseline financial motivation. Future research incorporating longitudinal primary data and experimental designs would strengthen causal inference regarding the long-term effects of interactive financial literacy tools.

Conclusion

The diffusion of financial literacy through interactive FinTech applications marks a significant transformation in how financial education is delivered and experienced. Mobile accessibility, gamification, and personalized feedback embed learning directly into everyday financial decision-making, improving both engagement and behavioral outcomes. Evidence from Southeast Asia demonstrates the potential of these platforms to expand financial inclusion and empower underbanked populations.

While challenges related to digital inequality, ethical design, and regulatory oversight remain, interactive FinTech applications offer a scalable pathway for improving financial literacy in an increasingly digital economy. Continued collaboration among educators, policymakers, and developers will be essential to ensure that these tools are inclusive, secure, and pedagogically effective.

Declarations

Use of AI technology:

AI-assisted tools were used for language refinement and clarity during the preparation of this manuscript. The author takes full responsibility for the content, analysis, and conclusions presented in this work.

Conflicts of interest:

The author declares that there are no conflicts of interest.

References

Ahmad, A. (2025). Gamification of personal finance: A systematic literature review. Association for Information Systems Conference Proceedings. https://www.nasdaq.com/docs/2026/01/12/Gamification-of-Personal-Finance-A-Systematic-Literature-Review-(Ahmad-et-al-2025).pdf

Aristei, D., & Gallo, M. (2025). Financial literacy, robo‑advising, and the demand for human financial advice: Evidence from Italy. arXiv preprint. https://arxiv.org/abs/2505.20527

Bitrián, P., Buil, I., & Catalán, S. (2021). Making finance fun: The gamification of personal financial management apps. International Journal of Bank Marketing, 39(7), 1310–1332. https://doi.org/10.1108/IJBM-02-2021-0074

Cannistrà, M., De Beckker, K., Agasisti, T., Amagir, A., Põder, K., Vartiak, L., & De Witte, K. (2024). The impact of an online game‑based financial education course: Multi‑country experimental evidence. Journal of Comparative Economics, 52(4), Article 100XXX. https://doi.org/10.1016/j.jce.2024.08.001

Chen, H., & Volpe, R. P. (1998). An analysis of personal financial literacy among college students. Financial Services Review, 7(2), 107–128.

Choung, Y., et al. (2023). Digital financial literacy and financial well‑being. Journal of Financial Services Research. https://doi.org/10.1007/s10693-023-00394-2

Croitoru, I. M., Dragan, P.-P., Ignat, N. D., & Jumanca, R. (2025). Exploring financial literacy in higher education with the help of FinTech: A bibliometric analysis. FinTech, 4(1), 4. https://www.mdpi.com/2674-1032/4/1/4

Dicheva, D., Dichev, C., Agre, G., & Angelova, G. (2015). Gamification in education: A systematic mapping study. Educational Technology & Society, 18(3), 75–88. https://www.jstor.org/stable/jeductechsoci.18.3.75

Digital finance and financial literacy: Evidence from Chinese households. (2023). Journal of Banking & Finance, 156, 107005. https://doi.org/10.1016/j.jbankfin.2023.107005

Digital finance and innovations in financing for education. (2016). CGAP Research Brief. https://www.cgap.org/research/publication/digital-finance-and-innovations-in-financing-for-education

Filippin, M. E. (2025). Who’s in? Government policies and financial literacy in market participation. arXiv preprint. https://arxiv.org/abs/2506.12575

Fernandes, D., Lynch, J. G., Jr., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1889. https://doi.org/10.1287/mnsc.2013.1849

Frontiers in Education. (2024). Fostering financially savvy generations: Intersection of financial education, digital financial misconception and parental wellbeing. Front. Educ., 9, Article 1460374. https://doi.org/10.3389/feduc.2024.1460374

Ghadafi, E., & Andriotis, P. (2025). UK finfluencers: Content, reach, and responsibility. arXiv preprint. https://arxiv.org/abs/2505.01941

Gomber, P., Koch, J.-A., & Siering, M. (2018). Digital finance and FinTech: A conceptual framework and research agenda. Journal of Management Information Systems, 35(1), 220–265. https://doi.org/10.1080/07421222.2018.1440766

Hamari, J., Koivisto, J., & Sarsa, H. (2014). Does gamification work? A literature review of empirical studies on gamification. Computers in Human Behavior, 37, 302–314. https://doi.org/10.1016/j.chb.2014.05.019

Islam, K. M. A. (2024). The role of financial literacy, digital literacy, and financial self‑efficacy in FinTech adoption. Investment Management and Financial Innovations, 21(2), 370–380. https://doi.org/10.21511/imfi.21(2).2024.31

Kusuma, B., & Halim, R. (2024). Influence of gamified financial literacy training on saving behavior: Experimental study in Indonesia. International Journal of Educational Research. https://doi.org/10.1016/j.ijer.2024.102122

Lee, J., & Kim, D. (2023). Blockchain in financial education platforms: Enhancing trust and engagement. Journal of Educational Technology & Society. https://www.jstor.org/stable/26910234

Liu, H.-C., & Lin, J.-S. (2021). Impact of internet integrated financial education on students’ financial awareness and financial behavior. Frontiers in Psychology, 12, Article 751709. https://doi.org/10.3389/fpsyg.2021.751709

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. https://www.aeaweb.org/articles?id=10.1257/jel.52.1.5

Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380. https://doi.org/10.1111/j.1745-6606.2010.01173.x

Mackenzie, C., & Lutz, C. (2022). Evaluating mobile gamification for financial decision support. Journal of Behavioral and Experimental Finance, 35, Article 100620. https://doi.org/10.1016/j.jbef.2022.100620

Mayer, R. E. (2020). Gamification and learning science: A review of theoretical underpinnings. Educational Psychology Review. https://doi.org/10.1007/s10648-020-09545-8

Organisation for Economic Co‑operation and Development. (2020). OECD/INFE 2020 international survey of adult financial literacy. OECD Publishing. https://www.oecd.org/finance/oecd-infe-survey-of-adult-financial-literacy-2020.htm

Organisation for Economic Co‑operation and Development. (2023). OECD/INFE 2023 international survey of adult financial literacy. OECD Business and Finance Policy Papers, No. 39. https://doi.org/10.1787/56003a32-en

Panos, G. (2025). Gamification on financial conduct and behavioral traits. Behavioral Finance Review. https://doi.org/10.2139/ssrn.3941234

Panos, G. A., & Wilson, J. O. S. (2020). Financial literacy and responsible finance in the FinTech era. International Review of Financial Analysis. https://doi.org/10.1016/j.irfa.2020.101515

Playing to learn: Game‑based approach to financial literacy for generation Z. (2024). Entertainment Computing, 52, Article 100896. https://doi.org/10.1016/j.entcom.2024.100896

Rana, S., & Paul, J. (2021). Consumer behavior and FinTech adoption: A literature review and future research agenda. Journal of Retailing and Consumer Services. https://doi.org/10.1016/j.jretconser.2020.102365

Remund, D. L. (2010). Financial literacy explicated: Theoretical perspectives and definitions. Journal of Consumer Affairs, 44(2), 276–295. https://doi.org/10.1111/j.1745-6606.2010.01169.x

Shao, R., & Ross, H. (2015). Financial education as a public policy tool: Introduction and survey. Journal of Consumer Affairs. https://doi.org/10.1111/joca.12075

Statista Research Department. (2024). Global smartphone subscriptions worldwide. Statista. https://www.statista.com/statistics/330695/number-of-smartphone-users-worldwide

The role of FinTech and “edutainment” in financial education. (2022). International Review of Financial Consumers, 7(2), 27–33. https://doi.org/10.36544/irfc.2022.7-2.5

To, P. L. (2026). Enhancing financial literacy and management through goal‑directed design and gamification in personal finance application. arXiv preprint. https://arxiv.org/abs/2601.08640

Trinh Quang Long, Morgan, P. J., & Yoshino, N. (2023). Financial literacy, behavioral traits, and ePayment adoption and usage in Japan. Financial Innovation, 9, 101. https://doi.org/10.1186/s40854-023-00504-3

Volpe, R. P., Chen, H., & Pavlicko, J. J. (1996). Personal financial‑literacy among college students: Survey results and classroom implications. Financial Practice and Education.

ABOUT THE AUTHOR

No bio provided.

COMMENTS

No comments yet. How about you be a Star to Comment?